The opportunity zones (OZ) investment marketplace is moving quickly to organize the participants for investment activities. The key participants are investors with capital available for investment, and viable businesses ready to accept OZ capital in the execution of specific business plans. In between is the Opportunity Zone Fund, serving an intermediary function between investors and business investments. The time is ripe for new and existing businesses to assess the potential to inject OZ capital to finance start-ups, venture and development phases, high growth and relocation expansion plans, and special situation buyouts.

The new tax law passed in December 2017 inaugurated a creative and unique incentive program for all U.S. taxpayers to pool their capital for investment into business start-ups, and emerging and growth businesses located in, or relocating into, specific census tracts designated as OZ throughout the United States and its territories. This powerful capital investment program has the realistic potential to create long-term jobs and to spur targeted economic growth and development. While the OZ capital marketplace is in its infancy, now is the time for business owners and entrepreneurs, and their advisors and bankers, to evaluate the structure of this marketplace, and to consider the benefits and consequences of including OZ investment capital in the company's options for capital raising.

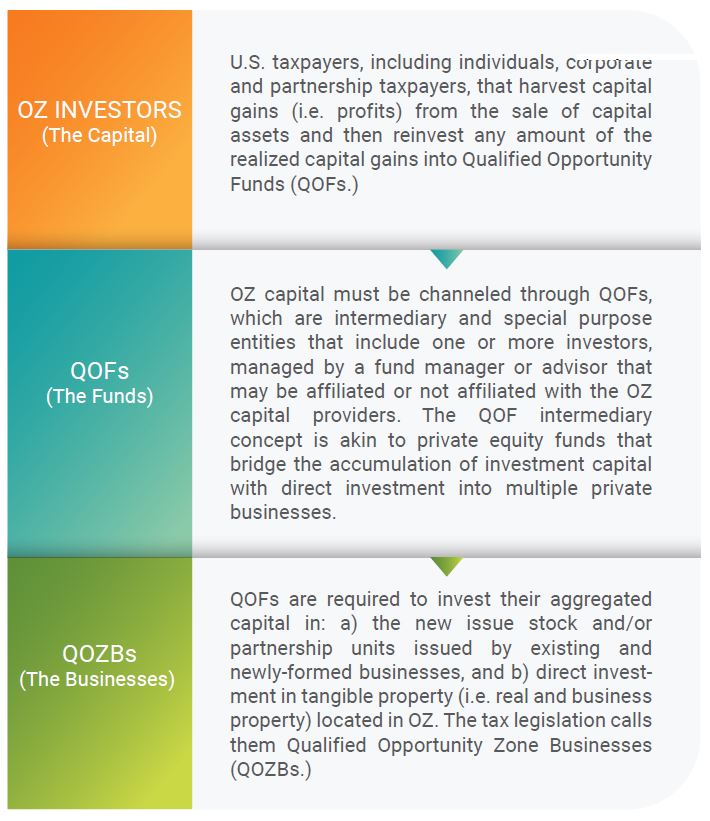

HOW THE OZ PROGRAM WORKS

It is worth repeating that in business, it is always imperative to know about your investors, partners and buyout counterparties. Accordingly, the key participants in the OZ capital marketplace can be simplified as follows:

OZ INVESTMENT IMPLICATIONS AND CONSEQUENCES

QOF FORMATIONS

QOFs currently in formation feature a variety of investment strategies, including: real property development and substantial renovation and/or investment in operating businesses, industry-specific businesses (e.g. solar energy), and specified geographic locations. The QOF formation process may be triggered in tandem with a specified investment, such as a new senior care facility, or a drone manufacturing plant seeking capital for relocation and expansion of manufacturing capacity, and then raising OZ capital through a QOF special purpose entity followed by a structured equity capital investment into the specified QOZB. Alternatively, QOFs are currently in formation to gather OZ capital into blind pool funds and then scour the markets to seek investments pursuant to specified investment strategies. So, either seek deals first and then seek OZ capital or raise OZ capital first and then seek deals.

QOF INVESTOR IDENTITIES

Business principals/entrepreneurs will interface with QOF managers/advisors in negotiating the investment terms and the conduct of due diligence processes for the direct injection of equity capital into their businesses. The capital providers may be known or unknown to the business principals, depending on the reverse transparency from the business investee to the QOF investors.

TAX-RELATED CONDITIONS ON OZ CAPITAL PROVIDERS

The OZ capital providers investing into QOFs are required to hold their QOF investment interest for at least ten years to be relieved of federal income tax liabilities on realized profits associated with the eventual sale or liquidation of their QOF investment interests. In other words, business principals and entrepreneurs can expect investment capital to be seeking durable and profitable investments with long-term horizons. However, it is common for private equity investment strategies to face a host of significant events, like recapitalizations, buyouts, mergers, workouts, and leverage that will need to be accommodated in the "normal" course of private equity investments. QOF investment and tax compliance rules will accommodate significant changes related to the QOFs’ investee businesses without jeopardizing the QOF investors’ anticipated tax benefits.

FEDERAL TAX COMPLIANCE PROGRAM IMPOSED ON INVESTORS AND BUSINESSES

OZ capital is neither a federal subsidy nor supported by federal guarantees. The program is created in the Internal Revenue Code (IRC) and U.S. taxpayers are in effect “supporting” the program by accepting the delayed collection of federal tax liabilities on short- and long-term capital gains and the forgiveness of federal taxes on capital gains for QOF investments held by QOF investors for more than 10 years. The OZ investment program features a rigorous federal tax compliance program to attach the tax benefits to private investment capital, and intersect with the investment deals between QOFs and the businesses receiving OZ capital to ensure the achievement of positive economic development benefits.

BUSINESS QUALIFICATION REQUIREMENTS TO ACCESS OZ CAPITAL

The OZ capital is sourced from the private capital markets, and yet the Internal Revenue Service has imposed some minimal requirements on the businesses that are positioning to access this long-term equity capital and to qualify as QOZBs. The minimal IRS requirements are summarized as follows:

• American businesses: Domestic corporations or domestic partnerships.

• In the zone: Headquarter location in OZ and “in situ” residency represented by real property ownership or market-rate leases employed in the QOZBs active trade or business after Dec. 31, 2017.

• Prohibited business activities: Not in the business of, or the provision of (including the provision of land for) any private or commercial golf course, country club, massage parlor, hot tub facility, suntan facility, racetrack or other facility used for gambling, or any store where the principal business is the sale of alcoholic beverages for consumption off premises.

• Demonstrated commitment to conduct business within the OZ: With respect to initial qualification and all subsequent years that the business is capitalized with OZ capital, then:

a. more than 70% of the business’ tangible property will be Qualified Opportunity Zone Business Property as defined in IRC Section 1400Z-2, and this 70% requirement is satisfied more than 90% of the time period that the OZ capital is invested in the business;

b. at least 50% of the business’ total gross income is associated with, and derived from, the active conduct of such business that itself is physically situated in OZ;

c. at least 40% of the business’ intangible property is used in the active conduct of such business that itself is physically situated in an OZ; and

d. less than 5% of the average of the aggregate unadjusted basis of the property of such business is classified as nonqualified financial property.

• Issuance of Corporate Securities for Cash: The business issues equity securities (corporate shares or partnership units) for cash, and at the time the equity securities are issued, the business is already in compliance with all of these qualified OZ business requirements, or, in the case of a newly-formed business, such business is being organized for the purpose of qualifying as a QOZB.

While these requirements may not appear to be onerous, it is imperative for business principals and entrepreneurs to assess their future business outlook to ensure that the continuous OZ requirements are consistent with growth-oriented business plans, to determine whether some OZ capital requirements may create future constraints, and to identify now the options to alleviate those potential OZ capital-related constraints.

OZ CAPITAL FOR BUSINESSES

Long-term equity capital to finance business growth, expansion and buyouts is the reward for businesses with vision, upside performance and the ability to share returns with investment partners. The OZ program’s potential presents a new chapter in private equity capital markets by consolidating investors seeking appropriate risk-adjusted returns coupled with geographic targeting to fuel economic development and job growth.

The OZ capital marketplace features the following potential benefits for businesses:

• An innovative channel to increase the amount of private equity capital from tax-motivated investors willing to inject capital into well-managed businesses with strong business plans coupled with viable exits strategies after long-term investment periods;

• Expands the dialogue between investors, businesses, and their respective advisers to evaluate and strategize on the wide range of private business investment opportunities- including start-ups, early stage venture capital, growth stage capital for proven businesses, and capital deployed in connection with strategic buyouts;

• Enables businesses to expand their capital base beyond the limitations imposed by self-financing, friends and family members; and

• Leverages on the preferences among OZ investors to achieve meaningful social and economic impacts within their investment strategies.

Businesses interested in pursuing OZ capital need to assess their readiness, prepare their business plans and organize their strategic processes in approaching the numerous and emerging Qualified Opportunity Funds. A web search for “Qualified Opportunity Zone Funds” will result in a number of OZ funds and OZ fund directories to give business principals a sense of this fast-moving capital marketplace. The majority of OZ funds are dedicated to real property development, but others are forming to be launched by for-profit and non-profit fund sponsors over the next six to 18 months with a focus on investing in operating businesses such as OZ Operating Businesses Funds, OZ Venture Capital Funds and OZ Hybrid Funds.